Two Shovels for the Same Mountain: Palantir vs. Databricks in Healthcare

And the next features each one needs to actually break ground

Healthcare has a data mess. Everyone admits it. Few build for it.

Two companies have built the most credible shovels on the market and they’re aimed at different parts of the same mountain. Palantir runs the operational layer of hospitals and federal agencies. Databricks runs the engineering and ML substrate for payers, providers, and pharma. The interesting twist of 2025 wasn’t that they started competing harder. It was that they signed a partnership and started selling each other.

If you work in healthcare AI, as a clinician, data engineer, product lead, or buyer, you need a clear-eyed map of where each one wins, where they collide, and what they should build next. Here it is.

Where Each One Stands Today

Palantir: the operational brain

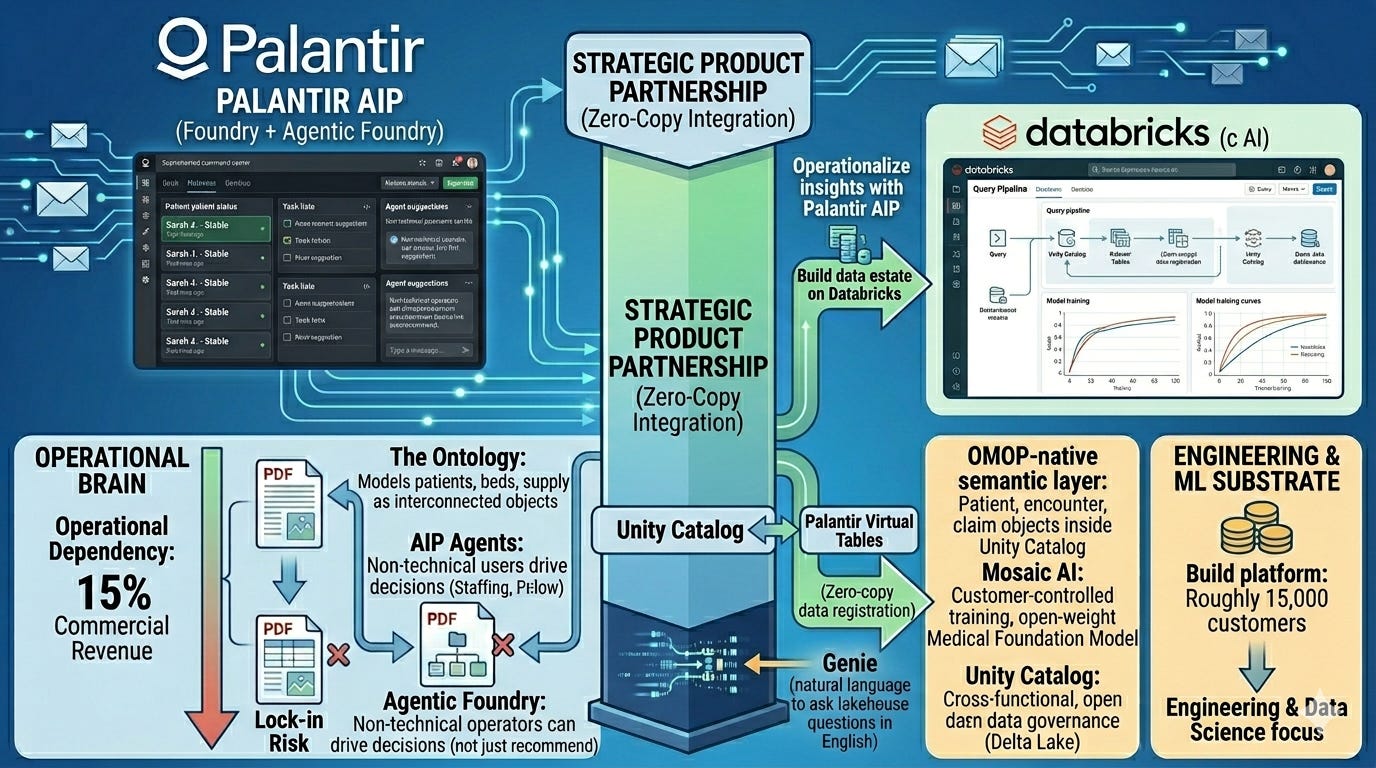

Palantir’s healthcare footprint is no longer experimental. AIP contracts now run at Cleveland Clinic, Tampa General, HCA, Mt. Sinai, MaineHealth, Option Care Health, and the NHS in England. Healthcare contributes roughly 15% of Palantir’s commercial revenue, sitting on top of a $702M commercial book in 2024. Federally, Palantir holds the SHARE blanket purchase agreement with HHS, runs Foundry across NIH, CDC, FDA, and ARPA-H, and is a finalist for the National Directory of Healthcare Providers.

The product moat has a name: the Ontology. Foundry doesn’t just store rows, it models hospitals as interconnected objects: patients, beds, encounters, claims, providers, supply items. AIP layers LLM-powered agents and workflows on top of that ontology so non-technical operators can drive decisions: patient flow, staffing, supply chain, revenue cycle. The new Agentic Foundry lets agents take actions, not just recommend them.

The pitch to a hospital COO is simple: we don’t sell you another dashboard. We restructure how decisions get made. That’s also why the contracts are sticky and why critics worry about operational dependency.

Databricks: the data and AI substrate

Databricks took a different path. Its Data Intelligence Platform for Healthcare and Life Sciences (formerly the Lakehouse) is built around the open Delta Lake format, Unity Catalog for governance, and Mosaic AI for model training and serving. The customer list reads like a different industry slice: Regeneron, GE Healthcare, ThermoFisher, Walgreens, Cognoa, plus most of the top-20 pharma names.

The wins are quantifiable. Regeneron compressed genomic data processing from 3 weeks to 5 hours, and genotype-phenotype queries from 30 minutes to 3 seconds, on workloads scaling to 1.5M exomes. Solution accelerators ship for disease risk prediction, digital pathology, OMOP-mapped real-world evidence, and FHIR ingestion via partners like John Snow Labs and ZS Associates.

Where Palantir wins the COO, Databricks wins the CDO, the head of data science, and the genomics team. Roughly 15,000 customers versus Palantir’s ~849, with consumption-based pricing that lets a 10-person team start without a six-figure contract.

The Competition: Less Head-to-Head Than You’d Think

The investor narrative wants a cage match. The reality is messier.

They overlap at the edges, not the core. Databricks is a build platform: data engineering, ML training, lakehouse storage, governance. Palantir is a deploy platform: ontology, operational apps, agentic workflows for non-technical users. Most healthcare enterprises that buy one eventually need the other.

Then came the partnership. In April 2025, the two companies announced a strategic product partnership. By late 2025, 100+ joint customers were already running production workflows on the combined stack. The technical bridge is zero-copy integration: Unity Catalog and Palantir Virtual Tables let data governed in Databricks register directly into Foundry without ETL or duplication. R1 RCM publicly stated that the partnership powers their healthcare revenue OS.

The translation for healthcare buyers: build your data estate on Databricks, then operationalize it through Palantir AIP. The lock-in fight got partially defused. The competition shifted from which platform wins your data to which platform owns the workflows your clinicians and operators touch every day.

That’s still a real fight. And it’s where the next product roadmap matters.

What Palantir Should Build Next

Palantir’s strength is operational depth. Its weakness is that healthcare is more than hospital ops. Three moves would unlock the next leg.

1. A native, FDA-clearable clinical decision support layer. AIP today optimizes patient flow, staffing, and revenue cycle, and administrative wins. The harder, more defensible play is regulated clinical AI: sepsis prediction, deterioration scoring, oncology pathway recommendations. This means a SaMD-ready submodule with model cards, drift monitoring, audit trails, and pre-built FDA 510(k) and PCCP documentation. Epic and Oracle Health are eating this from the EHR side. Palantir has the ontology to do it across health systems, not just inside one EHR.

2. A payer ontology and value-based care toolkit. Provider ops is now a crowded space. Payer ops, like claims, prior auth, network adequacy, risk adjustment, or MLR optimization, is where the margin lives. A pre-built payer ontology plus AIP agents for prior-auth automation and STARS optimization would extend AIP into the other half of the dollar. Bonus: it pairs directly with the Cognizant/TriZetto partnership announced in February 2026.

3. Patient-facing agentic workflows. Every Palantir workflow today targets the operator, not the patient. A HIPAA-compliant patient agent, like appointment scheduling, prep instructions, medication reconciliation, or discharge follow-up, sitting on the same ontology as the hospital’s command center would close the loop. It’s also the only credible way Palantir competes with the consumer-AI giants who will inevitably push into care navigation.

What Databricks Should Build Next

Databricks owns the substrate. Its weakness is that substrate doesn’t drive clinical adoption. Three moves would change that.

1. A clinical-grade ontology and semantic layer. Lakehouse + Unity Catalog is brilliant for engineers, opaque for operators. The Palantir partnership solves this by renting the ontology layer. That’s a strategic risk. Databricks needs its own healthcare semantic layer, OMOP-native by default, FHIR-aware, with pre-built object models for patient, encounter, claim, provider, and care episode, that lives inside Unity Catalog and powers Genie’s natural-language queries. Make it open. Then non-technical users don’t need Foundry to ask the lakehouse a question in English.

2. A regulated foundation model for medicine. Databricks acquired MosaicML to train custom foundation models. Healthcare needs this badly: a medical foundation model, trained on de-identified clinical text, imaging, and genomics, with documented training provenance, evaluation on standard clinical benchmarks, and a clear path to FDA-regulated deployment. Open-weight. HIPAA-deployable in a customer’s own VPC. Nothing on the market today combines clinical performance, transparency, and customer-controlled deployment. This is Databricks’ shot.

3. A clinical trials acceleration suite. Pharma is already Databricks’ strongest healthcare vertical. Going deeper means a vertical product for decentralized clinical trials: real-time site monitoring, AI-driven patient matching across EHR and claims data, automated CSR drafting, and regulatory submission packaging for FDA and EMA. ROI is measurable in weeks of trial timeline saved, which is the only metric pharma CFOs care about.

The Systemic Pattern

Step back from the platforms and a pattern emerges.

Healthcare AI is bifurcating. One layer is engineering; pipelines, models, governance, and scale. The other layer is cognition; how decisions actually get made by humans inside workflows. Databricks dominates the first. Palantir dominates the second. The 2025 partnership was an admission that no single vendor will own both within the decade.

For builders and buyers, the practical implication is clear: stop asking “Palantir or Databricks?” Start asking “where in my decision stack does each one fit?” Engineering teams pick Databricks first. Operations and clinical teams pick Palantir first. Mature health systems will run both, connected by the zero-copy bridge.

The companies that will win the next phase aren’t the platforms. They’re the vertical health-AI builders who use these shovels to dig real clinical and operational value, such as sepsis models that actually save lives, prior-auth agents that actually cut denials, or trial-matching engines that actually shave months off recruitment.

The Shovel for This Week

If you’re evaluating either platform right now, run this 4-question gate before any RFP:

Who is the primary user of the workflow? Engineer → Databricks. Operator/clinician → Palantir.

Is the bottleneck model-building or decision-making? Build → Databricks. Decide → Palantir.

Do you need regulated, audited operational AI in 90 days? Palantir’s Bootcamp model is unmatched here.

Do you need open data formats and avoid lock-in? Databricks’ Delta Lake is the only honest answer.

If you answer “both” to most of them, and most large health systems will, the partnership architecture is your real path. Stand up your data estate on Databricks. Operationalize it through Palantir AIP. Connect via Unity Catalog and Virtual Tables.

Two shovels. One mountain. Pick up both, but know which one is in which hand.

If this map helped, forward it to one operator or one engineer who’s stuck choosing between the two. They probably don’t have to.